Key points to remember:

- Circle Chief Economist Gordon Liao proposed raising USDC’s Aave V3 Slope 2 rate to 50% to restore liquidity after a KelpDAO exploit.

- A $292 million KelpDAO rsETH bridge attack on April 18 drained Aave of up to $15.1 billion in TVL in a matter of days.

- Aave’s USDC pool remained at 99.87% utilization for four days, with less than $3 million available liquidity to April 22.

Circle Chief Economist Proposes Higher USDC Rates on Aave V3 to Be Restored Liquidity After operating KelpDAO

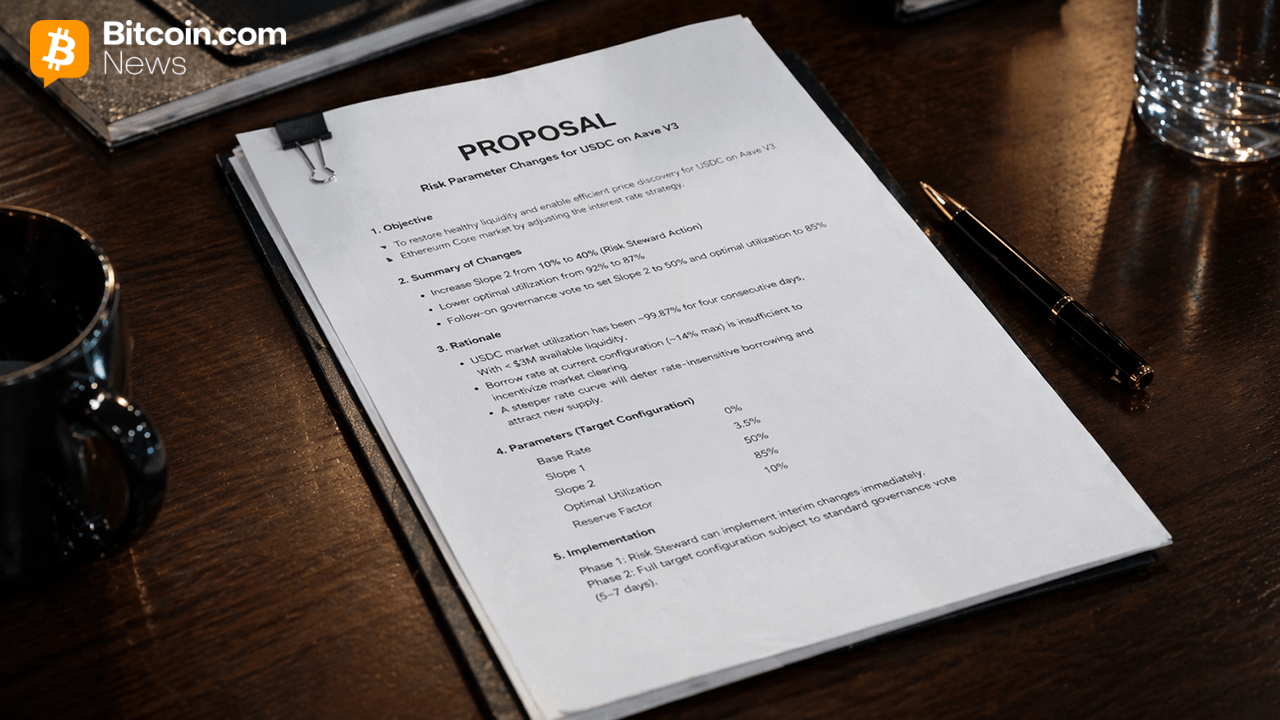

THE proposalfiled as Aave’s Request for Comment, requests Aave’s Risk Steward to immediately increase Slope 2 from 10% to 40% and reduce optimal utilization from 92% to 87%. A subsequent governance vote would push Slope 2 to 50% and optimal utilization to 85%. At 100% utilization under target configuration, USDC borrowers would face a maximum rate of around 53.5%, compared to the current cap of around 14%.

Liao, who stressed that his views were personal and not official Circle policy, linked the proposal directly to the April 18 KelpDAO rsETH exploit. Attackers exploited a vulnerability in KelpDAO’s bridge to siphon unbacked rsETH, post it as collateral on Aave V3, and borrow between $200 million and $300 million in assets, including WETH and stable coins. Aave froze the rsETH markets on V3 and V4 to limit further damage, but not before triggering what became a widespread backlash. liquidity crisis.

The consequences were serious. Aave’s total value locked (TVL) lost billions in a matter of days. The main markets, including ETH, USDTand USDC reached 100% utilization, effectively trapping depositors’ funds. Some users resorted to borrowing stable coins like GHO, DAI and USDe to access liquidity indirectly.

The USDC pool has become a focal point. According to Aavescan data as of April 22, total supply and borrowing each stood at nearly $1.89 billion, with funds available liquidity less than $3 million. The pool had been stuck at around 99.87% utilization for four days, with variable borrowing rates capped at nearly 13.82% and offering rates around 12.42%.

Liao’s proposal considers the post-kink flat rate as the central problem. Since the current Slope 2 is low, rate-insensitive borrowers treated the roughly 14% cost as a fee for bypassing queues rather than as an exit signal. The result was a market that failed to clear even as depositors attempted to exit.

According to Liao, sharply increasing the slope would provide price discovery, deter borrowers indifferent to rate levels, and attract new USDC supply within hours. He cited the Treasury and federal funds repo markets as a precedent for how steep curves solve short-term problems. liquidity dislocations.

Circle CEO Jeremy Allaire publicly shared the proposal on X, drawing greater attention to the governance discussion. Risk management service providers Lamarisk and Aave Labs have been identified as expected key participants.

The price of AAVE’s token fell by around 20-26% in the days following the exploit, amid the wave of releases. The governance proposal was interpreted by some market observers as a signal of stabilization.

The KelpDAO incident did not compromise GhostIt is smart contracts directly. The vulnerability originates from KelpDAO’s cross-chain bridge infrastructure. But the episode revealed how unsecured collateral coming in via bridging exploits can generate bad debt at the protocol level, with estimates of irrecoverable losses ranging from $124 million to $230 million on Aave markets, depending on how the losses are ultimately distributed.

Aave has published an rsETH incident report outlining recovery paths. Discussions on possible absorption of bad debts through mechanisms such as stkAAVE reduction are ongoing.

Liao’s two-stage approach keeps Slope 1 at 3.5%, base rate at 0%, and reserve factor at 10% unchanged. The interim Risk Steward action could take effect the same day if approved, while the full target configuration requires a standard five to seven day governance vote.